Hi there. Thanks for stopping by. I hope you had a splendid start into the New Year and wish you all the best for 2017!

I want to share with you some achievements we made in 2016 in regard of our savings rate. Read more… »

Hi there. Thanks for stopping by. I hope you had a splendid start into the New Year and wish you all the best for 2017!

I want to share with you some achievements we made in 2016 in regard of our savings rate. Read more… »

Can an investment in a solid and attractive – but “maturing” – company deliver decent returns despite slowing dividend growth?

Yes. But it is extremely important not to overpay and to take a long term view.

There are several wonderful businesses in my investment portfolio where I expect future growth to be weaker than in the last decades. I think in particular of Coca Cola, Nestlé, Novartis and Roche.

The Swiss company Roche has a market capitalisation of well above USD 200 Bn and is one of the largest pharma and biotechnology businesses in the world. It’s just massive!

In 2011, I acquired 18 non-voting shares of Roche at a price of around Swiss Francs 135 (CHF; trades more or less at parity to the USD).

Few weeks before I made that investment, shares of Roche had become kind of “unpopular” due to some damped expectations regarding profit contributions of one of its blockbuster drug. The stock price came down by around 20 %, making an investment even more attractive to me.

The worries of the market proved exaggerated, Roche delivered solid results and stock price quickly recovered. In the last four years, the trading range was between CHF 230 and 280.

I don’t focus too much on the stock price or book gains/losses regarding my investments, but it is still interesting to see how some short term market expectations can lead to quite a nice entry price.

Much more important for me is the cash flow I get in form of dividends.

When I make an investment, I want to see at least these two things over time:

If a stock investment does not meet (or excel) these two criteria, it does not contribute to my wealth building process.

The dividend payments in that time period were as follows (in CHF; gross amounts before witholding tax): 3.00, 2.50, 4.60, 5.00, 6.00. The payouts doubled in just five years which is very strong.

If someone had bought Roche in 2005 and is still holding that investment, he or she would have been rewarded handsomely in the past and will be so spectacularily in the future.

From 2005 to 2015, Roche showed a dividend growth rate of well above 14 %. But there are two crucial points to consider:

From 2011 to 2015 the dividend payments (in CHF; gross amounts) from Roche were as follows: 6.80, 7.35, 7.80, 8.00, 8.10. The 5 year dividend growth rate was around 5.9 %, much less than in the past.

My investment in Roche falls exactly in that slow growth period.

Fair enough. Let’s have a look at the development of the yearly cash returns compared to my initial investment of CHF 135 in 2011 (yield at cost). The deduction of the Swiss witholding of 35 % has hereby to be considered (if there is a double taxation treaty with the country of the investor, twenty percentage points can be reimbursed to that investor to lower the tax rate to 15 %).

My dividend yields at cost (after witholding taxes) from 2011 to 2015 were as follows: 3.25 %, 3.54 %, 3.75 %, 3.85 %, 3.9 %.

I expect my dividend yield at cost for 2016 (paid in 2017) to be well above 4 %. In the last five years, I collected over 18 % of the invested amount in dividends.

These are quite decent returns so far (I don’t even factor in the book gain or dividend (re-) investments).

Just to put the dividend returns into relation: The dividend yield of my total portfolio currently stands at around 3.3 %, “organic growth” due to dividend hikes of my holdings has been between 3 % and 4 % in the past years. So Roche was an important contibutor to “organic growth” of my portfolio and I expect it to be so in future.

Roche is a leader in biotechnology, cancer treatment and diagnostics. The company shows a 28 years of consecutive dividend growth. The business has a broad economic moat and shows strong fundamentals and attractive growth prospects.

The increasing payout ratio of Roche shows that EPS growth didn’t catch up with dividend growth. For decades, the payout ratio was low (under 20 %) and “jumped” above 40 % in 2003. Since the financial crisis starting in 2007 the payout ratio climbed steadily to settle currently at around 55 %. Still quite comfortable. Dividends are very well covered by free cash flow and there is some room for growth. But I expect dividend growth hikes to be modest in the future.

As a long term investor I don’t complain about that. A slowing payout is even prudent by the company.

I will rather have a look whether

Stocks of an outstanding company such as Roche acquired at a fair price can still deliver very decent returns over time. And if dividends are reinvested, the compound effect can do miracles.

Disclaimer

You are responsible for your own investment and financial decisions. This article is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

Drawing by the blogauthor

We have a wonderful custom in our family. Every year at Christmastime we watch the film “Mary Poppins”.

It’s a lovely musical fantasy comedy, produced by Disney in 1964. The main character, Mary Poppins, is a magical woman who descends from the clouds after having received an advertisement from the family Banks searching for a nanny to look after the two children Jane and Michael.

The wonderful messages in the dialogues and songs of the film are timeless:

Hi there, thanks for stopping by!

As promised in my latest blogpost Passive Income Review 2016 and Preview I will to give you a brief overview on the stock purchases I made this year.

In 2016 I invested the amount of Swiss Francs 16’600 (CHF; trades more or less at parity to the USD) into stocks of following five companies: Coca Cola, Walt Disney, Diageo, HSBC and Bayer.

I target a year over year growth of my dividend income of at least 15 % whereas

According to my projection, the five stock investments I made in 2016 will increase my 2017 dividend income by at least CHF 500. I expect that amount to grow by around 7.5 % each year due to organic growth and dividend reinvestments.

In 2016, Bayer, Diageo (I collected one of two semester dividend payments in 2016) and HSBC (I collected two of the quaterly dividend payments in 2016) already contributed to my income in the amount of CHF 205. In 2017 I will get dividends from Coca Cola’s and Walt Disney’s for the first time.

Now my considereations regarding the stock investments.

In December, 76 shares were acquired at a price of USD 40.3.

I view consumer staples and health-care shares as the backbone of my investment portfolio. I took some exposure into cyclical sectors and raw materials in the last two years as I saw attractive oportunities. In the long run though I want to give my stock portfolio a more defensive shape. There are some companies in these sectors I find interesting (e.g. J.M. Smucker) but stock prices are yet not there where I would feel comfortable.

I’ve had an eye on Coca Cola for some years. The stock has been trading in a range between USD 38 and USD 48 since 2012. I saw USD 40 as an interesting entry price and put a corresponding electronic order which was executed in December 2016.

I am well aware that the phenomenal earning per share (EPS) and dividend growth of the last decades are not likely to be replicable, but Coca Cola is still a very solid business with attractive prospects. More than half a century the company increased its dividends year over year. I don’t view a stagnant stock price over some years per se as a bad thing especially not when you reinvest the dividends and benefit from the compound effect.

Coca Cola’s payout ratio stands between 60 and 70 % which is higher than the decades before. It is very obvious that EPS-growth did not not keep up with the dividend increases of the last few years.

But the company has a strong balance sheet which has even improved in the last years. Coca Cola is sitting on over USD 20 Billion in cash. So, plenty of options for acquisitions (like the bottling operations from SABMiller in Africa) and future growth.

In November, 40 Shares were acquired at a price of USD 91.8.

I had an eye on Walt Disney for months and wrote about the company in one of my blogposts in October 2016 (Disney is a wonderful company but is the Price fair?). Since then, the price came down quite a bit and I made the purchase slightly above USD 90. Certainly not cheap but I am fine with that price.

In June, 132 shares were acquired at a price of GBP 20.75

Spirits and beer producer Diageo is a consumer staples company I have been looking at for several months. It has a great product portfolio with brands such as Johnnie Walker, Smirnoff, Captain Morgan, Baileys, Guiness Beer etc.

Unsurprisingly, you almost never see that company becoming really cheap. There is a wide economic moat and growth perspectives look very promising to me. I consider my purchase as “acquiring a piece of an attractive business for a fair price”.

In June, 466 shares were acquired at a price of GBP 4.6

A relatively large portion of my investment portfolio already consists of bank stocks. From the perspective of a long-term dividend growth investor (I want to hold my investments for decades unless fundamentals significantly deteriorate) I have quite mixed feelings concerning banks. There are

I think the banking industry as a whole is one of the very few investment segments where shareholder value has been destroyed over decades.

Fair enough. When I saw the stock price of HSBC being beaten down ahead of the Brexit vote I just couldn’t resist. In my view, HSBC is one of the very few banks to consider as solid businesses to invest in, of course always under the condition that the price is right and that there is a sufficient margin of safety.

When I made the investment in May 2016, the stock price was significantly below book value and price earnings ratio looked attractive to me. HSBC’s debt profile is robust and the bank’s core capital has been significantly strengthened. In August 2016, HSBC announced to start a share buy-back plan in the amount of USD 2.5 Billion (to finish early 2017) and to hold dividends steady.

In January, 30 shares were acquired at a price of EUR 103.

Bayer operates in four segments: pharmaceuticals, crop science, animal health and consumer health with well-known brands such as Aspirin, Alka Selzer, Bepanthen, Elevit, Supradyn, Rennie etc.

Bayer showed good performance in the past with strong EPS-growth and nice dividend history.

I had an eye on the company all trough 2015 and was particularily pleased to see the stock price coming down from EUR 140 to around EUR 100 in January 2016 at the time when I entered the position.

In May 2016, Bayer publicly disclosed to make an all-cash offer of USD 62 Billion to acquire the agriculture company Monsanto. The offer was increased to USD 66 Billion when Bayer and Monsanto finally came to an agreement regarding the merger. The closing of the transaction is expected by the end of 2017. Over 85 % of the offered amount has to be financed by a combination of debt and equity. Bayer will carry over USD 40 Bn in debts after the merger and promised to start deleveraging quickly.

There is no doubt, that Bayer has a track record of sucessfully acquiring companies, but this is by far the largest one ever. Bayer knows when there is an attractive investment oportunity, but from a perspective of a shareholder I see some downsides:

As said, I take a long-term view in regard to my investments and unless there will be a severe recession (such as the last one we saw from 2007 to 2009) over the next years, the combined compay has the potential to deliver double digit EPS-growth in future and – hopefully – shareholders will be compensated appropriately for their patience.

What do you think about the companies I invested in? Which investments have you made in 2016? Feel free to share your thoughts.

Disclaimer

You are responsible for your own investment and financial decisions. This article is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

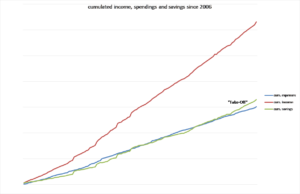

Just eleven days, and 2016 will be over. Time goes by so fast! It has been just an amazing year, I had a great time with my family and so much fun on our journey towards Financial Independence.

I want to share with you a brief look back to my passive income from dividends and interests which I have been tracking since 2012. I will also make some projections regarding future passive income streams.

As you can see, my two passive income sources developed quite differently. Read more… »