I have linked to the bullet points above articles resp. webstites on these Cryptos to provide some background information on their their applications, practical use, investment case etc.

Currently, I have roughly USD 4’000 invested in these four Crypto Positions.

If you put that amount into context to our other investments, it represents a small percentage.

So, Cryptos are hugely volatile and there is a significant speculative element inherently given, when taking a stake in that kind of asset. On the other hand, Bitcoin, Ethereum, Cardano and Ripple are connected with important applications which have huge potential to completely transform our economy and the way we interact.

I’ll keep you updated on how my new crypto investment portfolio has developed and how the positions have performed since they have been acquired.

What about you? Are you invested in Cryptos as well? Have you made any moves lately?

Thanks for sharing in the commentary section below.

Disclaimer You are responsible for your own investment and financial decisions. This article is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

or a great deal of luck in life (e.g. a windfall which would put these people financially in a positon so that they can leave their job).

Over the last decade, I have been extremely interested in personal finance in general and in the topic Financial Independence Early Retirement (FIRE) in particular.

By the way, I am referring here to a household’s wellbeing in general. Not everyone wants to achieve Financial Independence.

But in case you want to become financially independent in 10 to 20 years, that’s perfectly possible. Yes, the higher your wealth and/or your salary is, the easier it might be.

But here’s the catch: I high income could also make it even harder.

On MyFinancialShape I often write about establishing an ever growing passive income stream by investing into dividend paying stocks such as Nestlé, The Coca Cola Company, PepsiCo etc. I document our monthly cash flow streams from our investment portfolios. I write about some of the best long term dividend stocks, about dividend reinvestments and on taking advantage of the compound effect to accumulate substantial wealth over time.

But in essence, when we are talking about achieveing Financial Independence, it really just boils down to the Savings Rate.

A positive Jaws Ratio reduces risks, enhances profitability and flexibility

Mister Money Mustache wrote a brilliant article with the title Frugality as a Muscle. I highly recommend his blog in general and to have a look at that article in particular.

Here’s your “workout to gain financial muscles” that I would recommend:

know all your cost positons;

write them down, track them month by month in an excel sheet;

group the positions into fixed costs blocks (such as insurances, rent etc.) on one side and discretionary spendings (such as holidays etc.) on the other side;

analyse all cost positons and assess whether you could optimise them without significant disadvantages (these are the low hanging fruits);

discretionary spendings often can be influenced immediately but make sure you are cutting costs for things that don’t mean much to you;

get creative, many spendings positons could be altered quite easily (e.g. insurance shopping, improving costs by comparing, negotiationg, changing);

But always keep in mind: it’s absolutely important to remain motivated and enjoy the path toward Financial Independence as its a long term goal

tackle in particular the fixed costs because once they are streamlined, there is a recurring benefit. Fixed costs are always to the detriment of a household’s financial flexibility, as it takes most often six to 12 months to have an influence on them.

And here’s another point: if you can change your total costs faster than your income dynamic, then you are so much better off than litterally anybody you know.

And here comes the Jaws Ratio Concept which can have a life-changing effect.

I wrote an article How to use Jaws Ratio to improve finances some years ago. On how that concept – which originially has been used in the context of corporate finance and security analysis – could (and should) be applied in personal finance to optimise a household’s financial position over time. If you haven’t read that article, I would definitively recommend to have a look at it.

Jaws Ratio = Income Growth Rate – Expense Growth Rate

The Jaws Ratio can either be positive or negative depending on whether the income increase surpasses the expense increase or not. A positive result means that income grew stronger than expenses and therefore profitability increased.

I know people that got a pay rise, got promotions year after year which led to fast growing income. The savings rate was shooting up. But make no mistake: an increasing savings rate does not necessarily mean that your personal finances are healthy.

Here’s the flipside these people are often confronted with: if spendings have been climbing at a faster pace than income, then the household is in a very risky position.

As we all know, cash income streams can abruptly change, they can plummet dramatically or even stop completely. Just think of losing your job.

But costs always remain. It’s pretty tough cutting spendings in a matter of a few weeks, but it is completely feasible doing so over the medium and long run. As said, frugality is like a muscle which can and should be trained.

My wife and I have been applying the concept of Jaws Ratio for years. For instance, we reduced our work pensa from 100 % to 80 % while still keeping a more or less unchanged savings rate.

That was possible because we managed to slash our costs by more than the reduction of our work incomes. A 20 % salary drop should be accompanied by measures that lower the cost basis by at least 20 % which results in a Positive Jaws Ratio.

A Positive Jaws Ratio signifies

improved profitability of the household,

more flexibility and

also a lower risk profile.

But in contrast, when costs climbe faster than cash income streams that results in a Negative Jaws Ratio. It’s then vital to detect such a development at a relatively early stake and take measures. That’s why, the Jaws Ratio Concept really is so essential.

So, just track for each year, whether your income has been moving in line with your spendings. If that’s the case, put the process forward, make sure you always have a Positive Jaws Ratio and you are are seeing your journey towards gaining financial flexibility put on autopilot.

Over the first seven months of 2021, over Swiss francs 9’000 resp. USD 9’000 have been generated by our stock holding positions and Peer to Peer investments, which means that we achieved already 66 % of our annual passive income goal!

That’s quite good progress, compared to the first seven months in 2020, when our dividend portfolio experienced severe headwinds amid the COVID-19 pandemic and global lockdowns. In the comparable time period in the previous year, the sum of our passive income stood at USD 6’700. So in the current year passive income generation is significantly higher with + 47 % whereas a write-down of roughly USD 2’500 on our P2P in 2020 has to be taken into account.

Robust recovery on all fronts

In 2020, strong businesses had to cut or even eliminate their dividends, such as

French luxury giant Louis Vuitton Moet Hennessey (LVMH)

The Walt Disney Company

German car rental company SIXT etc.

I held all our share positions through 2020 and was even buying quite aggressively, adding many new stock holdings, in particular in the tech sector.

Going with great businesses through thick and thin and having a long term vision pays off handsomely. Investors are quite unforgiving when businesses cut their dividends.

But just look at the stock price dynamic of LVMH, The Walt Disney Company and SIXT:

But even some smaller companies in my stock portfolio have been able to capitalize on market disruptions amid the pandemic, such as German rental company SIXT.

Our portfolio not only has seen a very robust recovery in terms of book value, but also with regard to dividend payments.

LVMH for instance not only re-instated its shareholder distributions in 2021, but also hiked the dividend by 50 %.

Oil giant Royal Dutch Shell which drastically reduced its shareholder payouts in 2020 by a whopping 60 % is working hard to resume its dividends by increasing the distributions by 15 % and then by another 37 % in two consecutive quarters. We are still below the level of 2020, but things are moving into the right direction when it comes to the oil supermajors.

Fellow blogger European Dividend Growth Investor made a very interesting video plus post with the title Big Oil is back? A comparison of the 5 oil majors which you should check out if you are interested in the topic.

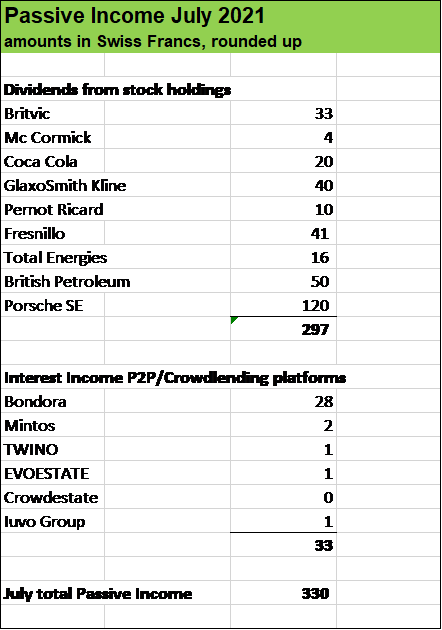

A brief look at our July Dividend Contributors

In July, nine businesses paid us the amount of CHF 297 resp. roughly USD 330.

British softdrink maker BRITVIC was hit particularily hard from the lockdowns and eliminated in 2020 its dividend but resumed its payout in 2021 which is definitively a good thing to see. Its stock price has recovered also nicely.

Let’s look at our other July dividend contributors.

The Coca Cola Company has been for years in my portfolio and of course has been hit by the global lockdowns. Consumption of beverages has been much lower in 2020 amid the closure of restaurants, bars, parks etc. But the giant is back on track and Free Cash Flow Generation has improved significantly. Another positive is the fact that The Coca Cola Company is further diversifying its product range.

Pernod Ricard is a French alcohol producer with a very strong brand portfolio, including Absolut Vodka, Havanna Club Rum, Malibu, Mumm Champagne, Martell Cognac etc. Due to its amazing grobal footprint and excellent management, Pernod Ricard navigated quite well through the international lockdowns and supply chain distributions, which is reflected in the stock price.

Mexican Fresnillo is the world largest producer of silver and Total Energies and British Petroleum (BP) are two of my oil supermajor positions. Total Energies has been particularily robust. BP has always shown an instable cash flow generation pattern but let’s not forget that this giant is still “digesting” the huge fine it has to pay for the oil spill in the gulf of Mexiko in 2010. In my view it’s quite probable to see BP’s cash generation stabilizing and grow in the years to come, which combined with a very attractive stock price and dividend reinvestments should make it a very interesting investment case.

Porsche Automobil SE is the main shareholder of the Volkswagen Group which itself has following ten car companies under its umbrella: Porsche, Audi, Lamborghini, Bugatti, Bentley, SEAT, Daccia, Ducatti, Man and Scania. I acquired stocks of Porsche SE years ago, in the midst of the so-called Diesel Crisis. Buying stocks of a solid business when it is experiencing some strong but not lethal pressure can pay off handsomely. The stock price has been climbing up through the years from around EUR 35 to almost EUR 100, and what’s best: Porsche Automobil Holding has been a very generous dividend payer through the years. Porsche Automobil Holding in essence just holds stocks of the Volkswagen Group plus a lot of cash. The shares trade at a discount to the market value of its holding position which can often be seen with that kind of businesses. See the Beauty of Holding Company Stocks.

What about you, fellow reader? How was your July in terms of investing and dividends?

Thanks for sharing in the commentary section below.

Disclaimer You are responsible for your own investment and financial decisions. This article is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

Our total stock investments with a market value of roughly USD 450’000 have moved higher by around 5 % in July alone. so a very nice boost to our wealth.

How about Cryptos in July?

The universe of Crypto Applications- and Currencies is huge.

Bitcoin (BTC or XBT) is the first ever Crypto. You can find further information on the history, applications and blockchain technology, Bitcoin Mining etc. in the articleWHY INVESTING IN BITCOIN.

Ethereum (ETH) in contrast to Bitcoin can do a lot more, for instance can it be used for smart contracts and decentralized applications. See also the article BUILDING THE INVESTMENT CASE FOR ETHEREUM.

Cardano (ADA) is a cryptocurrency network and open-source poject bult on the blockchain (see articleWHY INVEST IN CARDANO).

Currently, my Crypto portfolio has a market value of Swiss francs (CHF) 3’000 resp. around USD 3’300 whereas I am sitting on a book loss of roughly 23 %. or USD 700.

Currently, I am considering putting another USD 1’000 into Cryptos, equally distributed on the four current positions.

I’ll keep you updated how my new crypto investment portfolio has developed and how the positions have performed since they have been acquired.

What about you? Are you invested in Cryptos as well? Have you made any moves lately?

Thanks for sharing in the commentary section below.

Disclaimer You are responsible for your own investment and financial decisions. This article is not, and should not be regarded as investment advice or as a recommendation regarding any particular security or course of action.

Almost every household is confronted with that phenomenon: Lifestyle Inflation. It means that costs climb with income (for instance after a pay rise), all too often disproportionally.

What’s the problem with Lifestyle Inflation?

Well, it decreases the profitability of a household.

There is nothing wrong per se with consuming and enjoying an increasing salary, but there’s a flipside as climbing spendings often go hand in hand with a massively growing fixed cost block. This means people build up cost positions they cannot scale back in the short term.

For instance

renting a larger apartment leads to a higher rent

and higher costs for house insurance

as new furniture is bought etc.

The list goes on an on, and fixed costs are adding up really fast.

Fixed costs are to the detriment of the financial fexibility and stability of a household.

People tend to focus on discretionary spendings, such as going out to restaurants every week. These cost positions are low hanging fruits when someone wants to cut spendings to save money.

But let’s look at the fixed cost block and think about that: how fast could you slash your spendings for your rent and insurances if you lost your job or earned substantially less from one day to another? It could easily require months, even a year, to adapt your cost structure.

Eroding profitability of a household due to Lifestyle Inflation enhances its risk position and makes people stuck in a rat race having to work more and more just to pay their bills.

Lifestyle Inflation happens often slowly, over time, it’s a creeping process.

So how to tackle lifestyle creep and increase your financial shape?

It was a few years ago that I followed a conversation between two guys, one of them planning to buy a house for USD 1 Mio in a rural area.

That guy told his friend, that the down payment would be USD 250’000 and that he had saved that amount during the last 10 years. He said that his nest egg surpassed at least his “spending budget” of one year.

As the conversation went on, the future home owner said that – considering his high salary of USD 300’000 annually – his bank better offered him an attractive interest rate for the mortgage. After all, he added with a wink in his eye, he was now a millionaire.

That conversation showed a general misconception many people have on wealth and income.

Wealth is what you accumulate over time, not what you earn. The key factor in the process of wealth building is the saving rate. A high salary does not automatically translate into substantial wealth.